The Impact of Skyrocketing Mortgage Rates, Seller Strategies, and Inflation

Ever wondered why home prices are still reaching for the stars despite soaring mortgage rates and an economic landscape that seems to be hitting the brakes? In this blog, we unravel the mysteries behind the current housing market trends that have left home prices soaring to unprecedented heights.

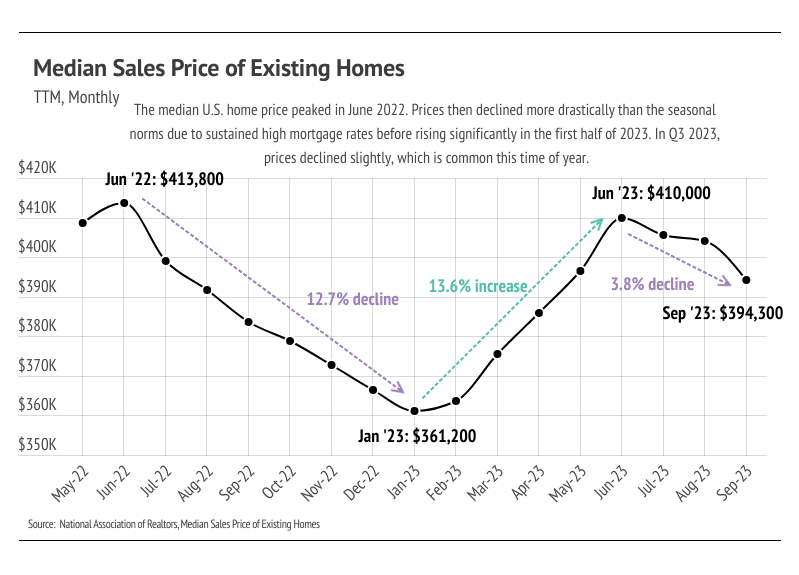

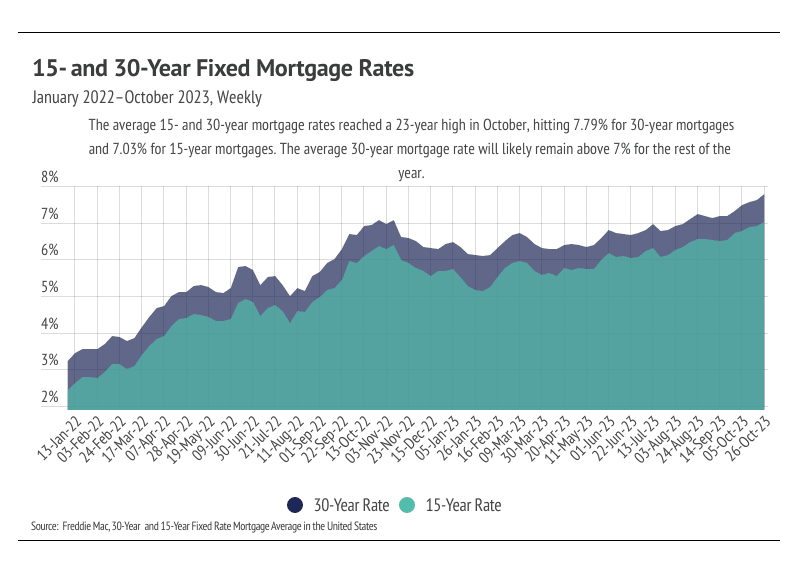

Home prices are still sky-high, mainly because there aren't enough houses to go around. Even though the average 30-year mortgage rate hit a 23-year high at 7.79% in October, the real troublemaker here is the rising mortgage rates. In simple terms, they're the main reason the housing market is slowing down. Let me break it down: the monthly cost for a typical home today is 11% more than in June 2022 when prices were at their peak. Zoom out a bit, and since the Fed started hiking rates in 2022, the monthly cost has shot up by a whopping 76%.

Now, you might wonder why prices haven't dropped, given this financial rollercoaster. Well, sellers want to keep prices high, or they won't bother selling. About 75% of U.S. homeowners have mortgage rates below 4%, thanks to JPMorgan. If prices take a nosedive, even fewer sellers would step into the market because they couldn't afford a new place with slim profit margins. Most sellers aren't selling because they have to; even breaking even on a sale isn't worth swapping a sub-4% mortgage for nearly 8%. Those entering the market now want to turn a profit to offset the higher mortgage rates. And this isn't just about existing homes – new construction faces the same song and dance. Builders deal with higher material and financing costs, and when it costs more to build, home prices rise.

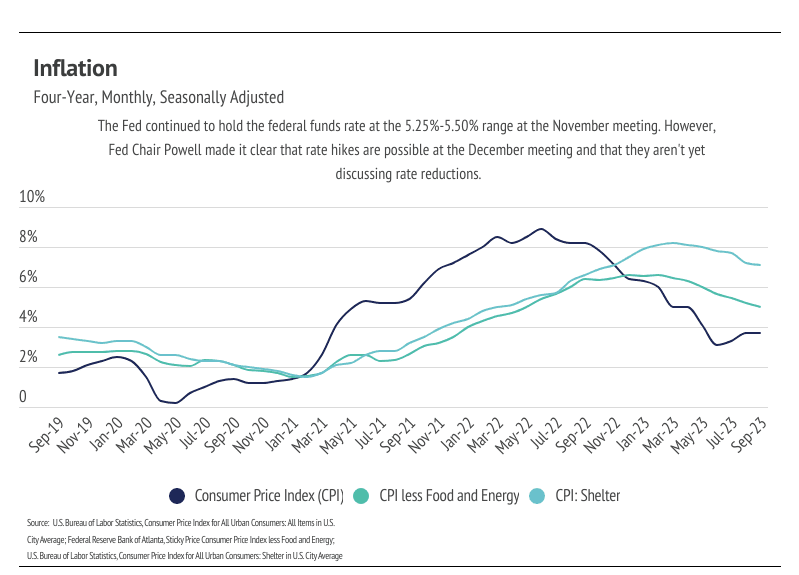

Inflation's another party crasher. People feel less wealthy because, in just three years from 2020 to 2023, the dollar lost 15% of its buying power, matching the loss of the previous 10 years. Inflation might be slowing down, but that just means prices are going up more slowly than before – not exactly a win for affordability. The combo of declining buying power and higher mortgage rates is like putting a brake on the market, making it move at a snail's pace.

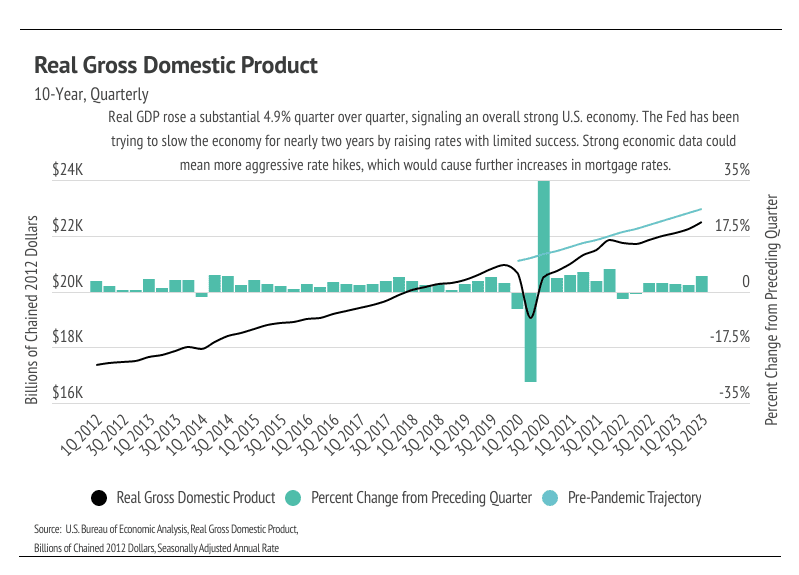

Hold on tight; those high mortgage rates are here to stay, thanks to inflation partying twice as hard as the Fed would like. The Fed's efforts to slow down the economy seem to be hitting the housing market the hardest. According to the National Association of Realtors (NAR), home sales dropped 2.0% monthly and a whopping 15.4% yearly – the lowest in four years. Real GDP is strutting its stuff in Q3 2023, showing robust U.S. economic growth, but the housing market is doing its own thing. Don't expect the Fed to change rates at the December meeting or anytime soon. Brace yourself for mortgage rates between 7% and 8% in 2024, keeping the market in a slow-motion groove.

Now, every region and house has its own story, so check out the Local Lowdown for a detailed scoop on your area. Generally, pricier spots like the West and Northeast are feeling the mortgage rate pinch more than the South and Midwest.

We've got our eyes on the housing and economic scenes to guide you through the maze of buying or selling your home. Whether you're a buyer, seller, or just curious about the pulse of the housing market, stay tuned for valuable insights and guidance. If you ever need assistance, don't hesitate to contact us. We're here to guide you in your real estate goals.

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.