Mortgage Rates Stabilize, Housing Market Seeks Recovery

The real estate market experienced stability in mortgage rates throughout January, with the Federal Reserve opting to maintain its benchmark rate. While hopes for rate cuts in March were somewhat dashed, the housing market is looking towards a potential recovery driven by consumer confidence. In this blog, we will delve into the current state of mortgage rates, the housing market's response, and the factors that may influence its future trajectory.

Mortgage Rates and Federal Reserve's Stance:

During its meeting on January 30th through 31st, the Federal Reserve decided to keep its benchmark rate within the range of 5.25% to 5.50%, which has been in place since July 2023. The Fed's cautious approach disappointed those advocating for rate cuts in March, but it indicates a preference for maintaining the current rate levels that seem to be working effectively. With inflation dropping and unemployment remaining low at 3.7%, the Fed's intention of achieving stable prices and low unemployment appears to be on track. While rate cuts may be delayed until mid-year, they may be considered if inflation continues to fall and economic indicators remain favorable.

Housing Market Response:

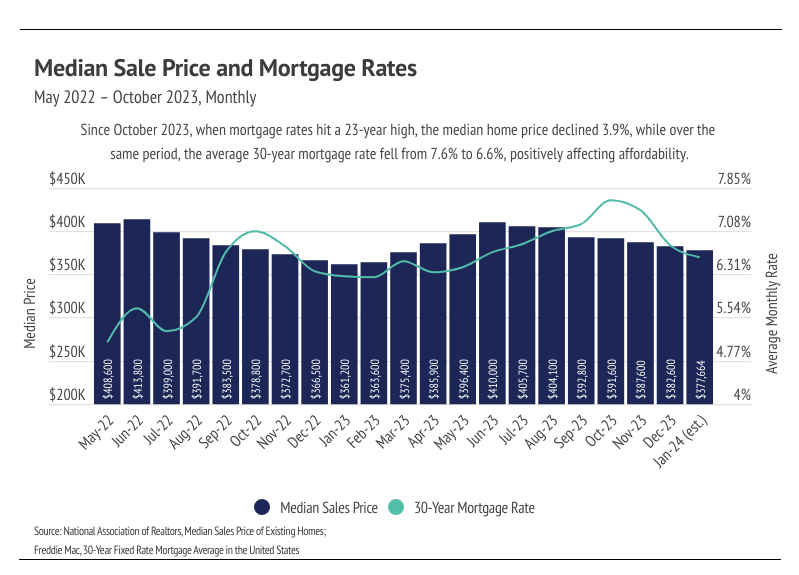

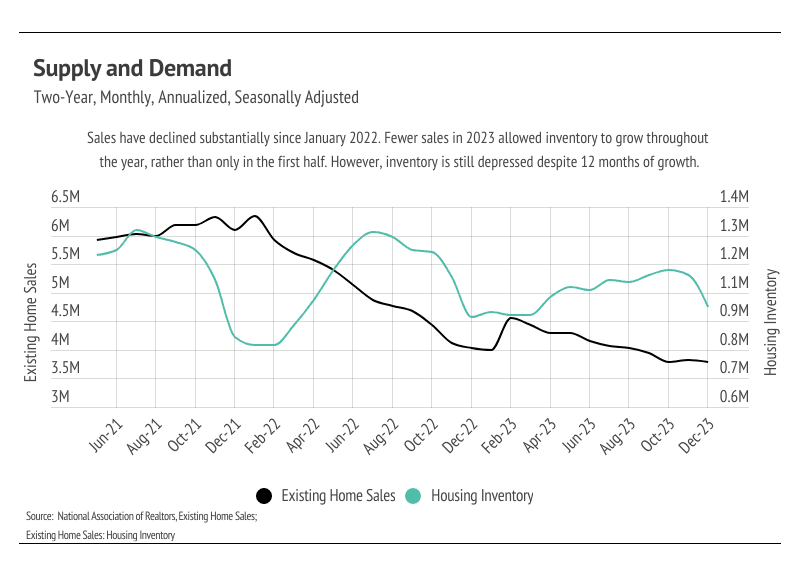

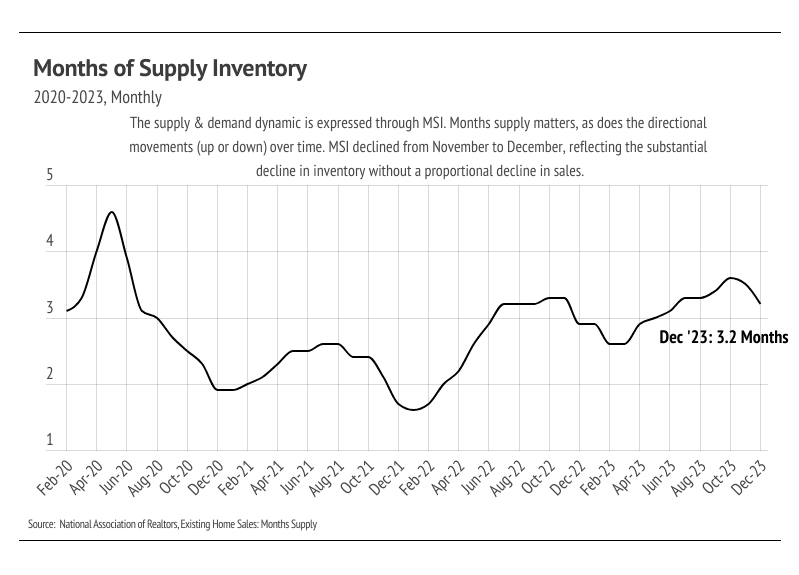

Following a significant drop in mortgage rates in November and December 2023, the housing market had the potential to warm up in the first quarter of 2024. However, the market's response has been slower than anticipated. Mortgage rates remained steady at around 6.5% in January 2024, which is still approximately 1% higher than the ideal rate to attract more participants to the housing market. Despite the decline in rates, sales reached a historic low, new listings were scarce, and inventory declined. While seasonal trends may explain some of these drops, the substantial rate decrease did not fully entice buyers and sellers back into the market. It is evident that rates need to decrease further to encourage greater participation.

Consumer Confidence and Earnings Growth:

A positive aspect of the current market is the recent improvement in workers' real earnings. After nearly a decade of earnings growth, followed by a decline due to the impact of COVID-19 and rising inflation, people's sentiment towards the economy was low. Dissatisfaction arose from the feeling of losing purchasing power and the inability to keep up with inflation. However, six consecutive quarters of real earnings growth have contributed to a more positive outlook on personal finances. This increase in consumer confidence is expected to benefit the housing market, as individuals feel more financially secure.

Regional Variations and Local Lowdown:

It's important to note that regional variations exist within the broader national trends. Higher-priced regions, such as the West and Northeast, have been more affected by mortgage rate hikes due to the higher absolute dollar cost and limited ability to build new homes. In contrast, less expensive markets in the South and Midwest have experienced less severe impacts. Understanding the local dynamics of your area is crucial for making informed decisions in the real estate market.

While the housing market seeks to recover, the stability of mortgage rates and the potential for consumer confidence to drive growth are key factors to monitor. As the Federal Reserve takes a cautious approach to rate cuts, the market's response may be delayed until mid-year. However, a further decrease in rates and continued growth in real earnings could positively impact the housing market. Stay informed about the local dynamics of your area and consult with real estate professionals to navigate the evolving landscape of the real estate market.

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.